import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from datasets import load_datasetKeywords

- EAR - Effective Annual Rate

- AUM - Assets Under Management

- MMF - Money Market Fund

- VaR - Value at Risk

- ARR - Average Rate of Return

1 Introduction

1.1 Background: The Evolving Landscape of Money Market Funds in Emerging Economies

Money Market Funds (MMFs) have emerged as preferred low-risk investment vehicles, particularly in emerging markets like Kenya, where financial awareness is growing and demand for reliable returns is increasing. These funds are structured as highly regulated pooled mutual funds that invest in short-term, high-quality debt instruments, often classified as cash equivalents. MMFs typically offer a compelling combination of capital preservation, high liquidity, and relatively predictable returns, making them attractive to both retail and institutional investors seeking a safe haven for their liquid assets (Step by Step Insurance 2025a; J.P. Morgan Asset Management 2023).

The global MMF industry has experienced substantial growth, reaching over USD 7.4 trillion, with institutional investors accounting for a significant portion of this total. Emerging markets have contributed notably to this expansion; for instance, the Chinese MMF industry has rapidly grown to USD 1.72 trillion, driven by both institutional and retail participation (J.P. Morgan Asset Management 2023). In Kenya, MMFs have become a go-to savings vehicle for risk-averse investors, pooling money from individuals and institutions for investment in ultra-safe assets like government Treasury bills and blue-chip corporate bonds (Step by Step Insurance 2025b). The Assets Under Management (AUM) for Kenyan MMFs have shown consistent upward trends, with a 5-year Compound Annual Growth Rate (CAGR) of 31.8% from Q2’2019 to Q2’2024, reaching Kshs 254.1 billion by the end of Q2’2024 (Cytonn Research 2024). By Q4’2024, MMFs held the largest investment allocation among Unit Trust Funds, totaling Kshs 246.8 billion, representing a 25.4% increase from the previous quarter (Cytonn Research 2025). This growth underscores their increasing importance in the Kenyan financial ecosystem.

The appeal of MMFs in Kenya stems from their ability to offer higher yields than traditional savings accounts (averaging 10-12% annually compared to 4-6% from banks), coupled with excellent liquidity, and some Fund managers processing transcation-free withdrawals instantly without limits on the number of withdrawals you can make in a day (Safaricom 2024). They are particularly suited for short-term financial goals, such as emergency funds, school fees, or temporary cash parking (Lofty-Corban 2025). Recent innovations, such as the Ziidi Money Market Fund, launched in partnership with Safaricom’s M-PESA platform, have further democratized access to MMFs. Ziidi MMF allows investments from as little as KES 100, offers free deposits and withdrawals via M-PESA, and accrues daily interest, attracting over 680,000 active investors and managing over KES 6.2 billion in assets by early 2025 (Step by Step Insurance 2025b). This mobile-first approach significantly enhances financial inclusion, particularly for low and mid-income earners, aligning with broader economic transformation agendas.

1.2 Problem Statement: Addressing the Limitations of Deterministic Metrics in MMF Evaluation

Despite their growing popularity and perceived safety, investors in Kenya’s MMFs often base their fund allocation decisions on limited, deterministic metrics, such as the last month’s Effective Annual Rate (EAR) or simple average annual returns (Step by Step Insurance 2025a). While seemingly straightforward, these single-point estimates inherently fail to capture the crucial variability and underlying risk of returns over time. This reliance on static indicators can lead to several critical shortcomings in investment decision-making.

\[ \text{EAR} = \left(1 + \frac{i}{n}\right)^n - 1 \]

Where:

- \(i\) = nominal annual interest rate (as a decimal)

- \(n\) = number of compounding periods per year

Firstly, the Effective Annual Rate (EAR), while useful for understanding the true cost or return of an investment accounting for compounding, has notable limitations. It assumes a constant interest rate throughout the year, which is often unrealistic in dynamic market conditions. Furthermore, EAR calculations typically do not account for additional fees, taxes, or charges associated with financial products, which can significantly impact the actual profitability. Market volatility and inflation can also cause the actual yield to deviate from the calculated EAR, eroding the purchasing power of returns (Sarah Lee 2025b).

Secondly, the Average Rate of Return (ARR) method, commonly used for initial screening, presents even more significant drawbacks for comprehensive risk assessment. It disregards the timing of cash flows, assuming all inflows and outflows occur simultaneously, thereby ignoring the time value of money (Jerry Grzegorzek 2022). Crucially, ARR does not consider the risk associated with an investment, potentially overestimating returns for high-risk ventures and underestimating them for low-risk ones (Dave 2024). This focus solely on accounting profits, which can be subject to manipulation, rather than cash flows, further limits its utility for robust decision-making. Such limitations mean that investors relying solely on these metrics may underestimate the true risk exposure or overlook funds that perform consistently within a favorable, yet less volatile, range (Jerry Grzegorzek 2022; Dave 2024).

Moreover, investor decision-making is susceptible to behavioral biases, such as overconfidence and herd mentality, which can be exacerbated by the simplicity of traditional metrics (Raymond A. Mason School of Business 2025). Overconfidence can lead investors to make high-risk investments based on an inflated assessment of their expertise, while herd mentality can cause decisions to be driven by group behavior rather than independent analysis, often resulting in market bubbles or panic selling. The lack of a decision-support framework that explicitly accounts for historical variability and projects the range of possible future outcomes leaves investors vulnerable to these biases and market fluctuations.

Therefore, there is a pressing need for a more sophisticated framework that moves beyond single-point estimates. By visualizing return distributions rather than relying on deterministic figures, investors can assess both expected gains and potential losses, enabling more resilient and risk-aware investment strategies in the dynamic Kenyan MMF landscape.

1.3 Research Objectives

The general goal of this study is to provide a robust, risk-adjusted performance evaluation of Kenyan Money Market Fund (MMF) schemes using Monte Carlo simulation.

To achieve this general objective, the study sets forth the following specific objectives:

- To preprocess historical Effective Annual Rate (EAR) data for Kenyan MMFs

- To model the statistical behavior of scheme-specific returns

- To simulate future return scenarios over a one-year horizon

- To visualize return distributions using statistical plots

- To identify MMFs with superior risk-return profiles to aid investor decision-making

1.4 Research Questions

The study aims to address the following research questions:

- How does the historical EARs of different MMF schemes in Kenya compare in terms of variability and risk?

- What are the projected future return distributions for these MMFs based on historical data?

- Which MMF schemes demonstrate the most favorable risk-return profiles, as indicated by their simulated return distributions?

1.5 Contribution of the Study

This study makes several significant contributions to the existing body of knowledge and practical application in financial markets, particularly within the context of emerging economies.

Firstly, it addresses a critical gap in the literature by applying Monte Carlo simulation specifically to Kenyan Money Market Funds. While Monte Carlo simulation is a well-established technique in global financial markets analysis, its application to less volatile instruments like MMFs, and particularly within the Kenyan market, has been limited. This research demonstrates the value of simulation-based analysis even for instruments perceived as low-risk, highlighting that MMFs are still subject to market influences such as interest rate shifts and macroeconomic fluctuations (Xu 2024a).

Secondly, the study provides a robust decision-support framework that moves beyond the limitations of traditional, deterministic performance metrics. By generating forward-looking probability distributions of returns, it offers investors a dynamic and comprehensive view of potential future outcomes, including downside risk, which is often overlooked by metrics like average EARs (Step by Step Insurance 2025a). This probabilistic approach empowers investors to make more informed, risk-aware decisions by understanding the full spectrum of possible returns, not just expected values.

Thirdly, the research contributes actionable insights for various stakeholders in the Kenyan financial ecosystem. For investors, it offers a nuanced understanding of risk-return trade-offs, enabling them to select MMFs that align with their specific risk tolerance and capital preservation goals. For financial advisors, it provides a tool for communicating complex risk profiles to clients more effectively through visualization. For fund managers, it emphasizes the importance of transparency in reporting not only historical returns but also metrics like volatility and simulated downside risk. For researchers and developers, it lays the groundwork for extending the framework to include additional macroeconomic variables or fund-specific strategies.

Finally, by utilizing a curated dataset of monthly EAR values for Kenyan MMFs, the study contributes to improving transparency in Kenya’s collective investment landscape (Kabui, Charles 2024). The methodology is lightweight, transparent, and fully reproducible using open-source tools, making it accessible for both institutional and retail applications. This work underscores the necessity of integrating risk-aware simulation techniques into everyday fund comparison tools, providing a more reliable and informative basis for investment decisions in emerging markets (Sarah Lee 2025a; KPMG Ghana 2024).

2. Literature Review

2.1 Money Market Funds: Structure, Evolution, and Role in Financial Inclusion

Money Market Funds (MMFs) are a cornerstone of the global financial system, designed as pooled mutual funds that invest in short-term, high-quality debt instruments (J.P. Morgan Asset Management 2023). Their primary objectives are capital preservation, high liquidity, and generating competitive returns relative to other cash equivalents (J.P. Morgan Asset Management 2023). MMFs typically hold a diversified range of securities from various issuers and maturities, focusing on instruments with the highest short-term credit ratings, such as Treasury bills, Certificates of Deposit (CDs), and commercial paper (Auerbach, Michael P. 2021). This diversification is crucial for preserving capital and ensuring liquidity.

The concept of MMFs originated in the late 20th century. The first MMF, Conta Garantia, was introduced in the Brazilian marketplace in 1968 by John Oswin Schroy. This was followed by Bruce R. Bent’s Reserve Fund on Wall Street in 1971, which brought the concept to a much grander scale (Auerbach, Michael P. 2021). Since then, the global MMF industry has expanded significantly, reaching over USD 7.4 trillion, with a substantial portion driven by institutional investors. MMFs have become popular not only in developed markets like the US and Europe but also across Asia and other fast-developing economies (J.P. Morgan Asset Management 2023).

Historically, MMFs aimed to maintain a stable Net Asset Value (NAV), typically $1 per share, using amortized cost accounting (J.P. Morgan Asset Management 2023). However, the financial crisis of 2008-2009 exposed vulnerabilities, as exemplified by the Reserve Primary Fund, which “broke the buck” (NAV fell below $1) due to holdings of Lehman Brothers’ commercial paper (Auerbach, Michael P. 2021). This incident led to widespread investor redemptions and necessitated government intervention to stabilize the industry (Kacperczyk and Schnabl 2013). In response, regulators introduced new guidelines and accounting methodologies, resulting in three main types of MMF NAV structures: Constant NAV (CNAV), Low Volatility NAV (LVNAV), and Variable/Floating NAV (VNAV/FNAV), each reflecting different risk and accounting approaches (J.P. Morgan Asset Management 2023).

In emerging markets like Kenya, MMFs play a vital role in financial development and inclusion. They serve as a crucial alternative to traditional savings accounts, offering higher yields and greater liquidity (Step by Step Insurance 2025a). The growth of MMFs in Kenya has been substantial, with Assets Under Management (AUM) consistently increasing. For instance, in Q4 2024, MMF AUM totalled Kshs 246.8 billion, accounting for 63.4% of all unit trust investments (Cytonn Research 2025), demonstrating their dominant position as a preferred investment choice. This preference is driven by ease of investing, high liquidity, and competitive returns.

A key aspect of MMFs’ role in financial inclusion in Kenya is their integration with mobile money platforms. The launch of Ziidi Money Market Fund, in partnership with Safaricom’s M-PESA, exemplifies this trend (Safaricom 2025, 2024). This initiative allows customers to invest from as little as KES 100, earn daily interest, and manage funds directly from their M-PESA wallets, thereby making wealth creation accessible to a broader segment of the population, including low and mid-income earners (Standard Investment Bank 2025). Such innovations are critical for deepening financial wellness and aligning with national economic transformation agendas that aim to empower more Kenyans financially.

2.2 Monte Carlo Simulation: Theoretical Underpinnings and Applications in Finance

Monte Carlo simulation is a powerful computational technique that leverages randomness to model and analyze complex systems and predict possible outcomes of uncertain events (Sarah Lee 2025a). Named after the famous casino city of Monaco, it was invented by John von Neumann and Stanislaw Ulam during World War II, initially for applications in nuclear science, such as understanding the statistical behavior of neutrons in nuclear explosions (Sarah Lee 2025a; Kenton 2025).

The theoretical foundation of Monte Carlo simulation rests on several key principles:

- Randomness and Probability: At its heart, the method involves performing a large number of simulations using random variables drawn from specified probability distributions (e.g., normal, uniform, triangular) to approximate a solution. This allows for the assessment of a wide range of possible outcomes under various conditions, capturing the inherent uncertainty of input parameters (Sarah Lee 2025a)

- Law of Large Numbers: The methodology is grounded in the law of large numbers, which guarantees that as the number of trials or simulations increases, the average outcome of the simulation will converge towards the expected value. This means that the accuracy of the results is directly proportional to the number of simulations performed (Sarah Lee 2025a)

- Reproducibility: Despite the use of random numbers, when the underlying probability distribution is accurately specified and the simulation is rigorously implemented (e.g., by setting random seeds), the results are both reproducible and statistically significant (Sarah Lee 2025a)

In finance, Monte Carlo simulation has become an indispensable tool for managing uncertainty, modeling complex markets, and evaluating policy decisions. Its applications span various domains, including:

- Risk Assessment: It is widely used to assess Value-at-Risk (VaR) and quantify how likely outcomes will deviate significantly from average predictions. By simulating potential market losses under extreme conditions, financial institutions can identify vulnerabilities and set capital adequacy ratios (Xu 2024b)

- Portfolio Optimization and Valuation: The method allows for simulating the performance of investment portfolios under a variety of market scenarios, providing quantitative evidence to support risk management and aid in portfolio valuation (Xu 2024b)

- Performance Forecasting: Monte Carlo simulation generates forward-looking probability distributions, offering a dynamic view of potential future outcomes for asset prices and investment performance, rather than relying on static historical insights (Xu 2024b; Sarah Lee 2025a)

- Derivative Pricing: It is an effective method for estimating the value of derivatives, whose prices are contingent upon the future prices of underlying assets subject to multiple random factors (Xu 2024b)

- Stress Testing: Financial institutions use Monte Carlo simulations for stress testing business performance under extreme market conditions, providing a foundation for robust risk management (Xu 2024b)

The process typically involves defining a mathematical model that links input and output variables, determining appropriate probability distributions for input values, generating a large sample dataset, running the simulation, and finally analyzing the results using statistical tools like histograms to visualize the output distribution. This approach provides a clearer, probabilistic picture compared to deterministic forecasts, especially when dealing with numerous interconnected risk factors.

2.3 Limitations of Traditional Performance Metrics and the Value of Probabilistic Approaches

Traditional fund evaluation metrics, such as trailing returns, average annual returns, or even the Effective Annual Rate (EAR), provide static insights that often overlook crucial distributional nuances and inherent risks. While seemingly straightforward, their deterministic nature presents significant limitations for comprehensive investment decision-making (Jerry Grzegorzek 2022; Dave 2024).

The Effective Annual Rate (EAR) is valuable for comparing interest rates with different compounding frequencies, reflecting the true cost or return over a year. However, its fundamental limitations include the assumption of a constant interest rate, which is rarely the case in volatile financial markets. EAR also typically excludes fees, taxes, and other charges, which can significantly distort the actual profitability of an investment (Sarah Lee 2025b). The impact of inflation can also erode the real purchasing power of returns, even with a high nominal EAR (@ Dave 2024).

Similarly, the Average Rate of Return (ARR) method, while simple, suffers from several critical drawbacks that undermine its effectiveness in risk assessment. A primary limitation is its disregard for the timing of cash flows, assuming they occur simultaneously, thus failing to account for the time value of money (Jerry Grzegorzek 2022). This can lead to inaccurate calculations, as the value of money changes over time due to inflation and interest rates. Crucially, ARR does not consider the inherent risk associated with an investment, potentially overestimating returns for high-risk assets and underestimating them for low-risk ones. Moreover, ARR relies on accounting profits, which can be manipulated, rather than more reliable cash flows (Dave 2024). It also fails to provide a clear indication of the payback period or opportunity cost of capital, which are vital for liquidity management and comparative analysis. Relying solely on ARR can encourage a short-term investment approach, potentially leading to the rejection of attractive long-term projects with initially lower average returns (Jerry Grzegorzek 2022).

These limitations of traditional metrics are particularly problematic because investor behavior is often influenced by cognitive biases (Raymond A. Mason School of Business 2025). Overconfidence bias, where investors overestimate their abilities, can lead to high-risk investments based on an inflated assessment of expertise. Herd mentality, driven by fear of missing out (FOMO), can cause investors to follow group behavior without independent analysis, contributing to market bubbles or panic selling. Prospect theory highlights loss aversion, where individuals feel the pain of losses more acutely than the pleasure of equivalent gains, influencing decisions to avoid selling losing assets. Regret aversion can cause investors to skip periodic portfolio assessments. When investment decisions are based on simplified metrics that do not fully capture risk, these biases are amplified, leading to potentially suboptimal outcomes.

In contrast, probabilistic approaches, such as Monte Carlo simulation, offer a superior framework for financial analysis by capturing the full spectrum of uncertainty and variability. By generating thousands of simulated future return paths, Monte Carlo methods provide forward-looking probability distributions, offering a dynamic view of potential outcomes (Xu 2024b). This allows investors to assess not just expected gains, but also the likelihood of various outcomes, including potential losses (tail risk), which is crucial for risk-aware decision-making (Sarah Lee 2025a). The ability to quantify uncertainty and visualize return distributions (e.g., through boxplots) enables a nuanced understanding of volatility and downside exposure, fostering more resilient investment strategies (Xu 2024b). This approach provides a more comprehensive and accurate picture of an investment’s true risk-return profile, mitigating the pitfalls associated with relying solely on static, deterministic metrics (Pavlik and Michalski 2025).

2.4 Money Market Funds and Financial Market Dynamics in Emerging Economies

Money Market Funds in emerging economies operate within unique financial market dynamics characterized by distinct opportunities and challenges. While MMFs globally are designed for capital preservation and liquidity, their behavior and evaluation in emerging markets like Kenya can differ significantly from developed markets due to varying economic stability, regulatory environments, and investor behaviors (KPMG Ghana 2024).

Emerging markets often present higher volatility and less predictable financial conditions compared to developed markets (KPMG Ghana 2024). This can be attributed to factors such as economic instability, limited access to capital, and the need for robust risk management strategies. For instance, currency fluctuations can significantly undermine profitability and financial stability for businesses in these regions (Ejiofor and Attah 2023). While MMFs are generally considered low-risk, even they are subject to market influences such as interest rate shifts and macroeconomic fluctuations (Lofty-Corban 2025). The Central Bank of Kenya (CBK) plays a crucial role in managing financial markets through monetary policy implementation, foreign exchange reserve management, and domestic debt management, which directly influence the environment for MMFs. Changes in government paper yields, for example, directly impact MMF returns, as these funds invest heavily in short-term government securities.

Investor behavior in emerging markets can also exhibit unique characteristics. While MMFs are popular for their low risk and liquidity, fund inflows can be highly responsive to fund yields, creating incentives for fund managers to take on more risk in pursuit of higher returns. This was observed during the 2007-2010 financial crisis, where MMFs, despite their perceived safety, expanded their risk-taking opportunities due to increased spreads between risky instruments and safe government securities. This highlights a potential vulnerability to runs, where illiquid assets backing demand deposits, coupled with stable NAV accounting, can lead to forced asset liquidation if market values drop (Kacperczyk and Schnabl 2013).

The regulatory environment, particularly the Capital Markets Authority (CMA) in Kenya, plays a vital role in overseeing MMFs. CMA reports provide crucial data on AUM growth and investment allocations, showing MMFs’ dominance in the Unit Trust Funds sector (Cytonn Research 2024). However, challenges in MMF evaluation in emerging markets can stem from data quality and completeness issues, as some schemes may exhibit flat or suspiciously low-variance return profiles, potentially due to stale or synthetic historical data. This necessitates robust data preprocessing and careful interpretation of results (Kabui, Charles 2024).

Traditional valuation methods, such as Discounted Cash Flow and Market Multiples, often fall short in emerging markets due to a lack of transparency, inefficiency, and significant economic, political, and social risks. The assumptions underlying models like the Capital Asset Pricing Model (CAPM), such as the availability of a risk-free rate and the efficient market hypothesis, may not hold true in these contexts (KPMG Ghana 2024). This further underscores the need for alternative, more robust evaluation techniques.

In this context, Monte Carlo simulation offers significant advantages. It can model complex, non-linear economic systems by capturing inherent randomness and variability, making it suitable for risk analysis and performance forecasting in volatile emerging markets (KPMG Ghana 2024). By quantifying uncertainty and providing probability distributions of potential outcomes, Monte Carlo methods offer a more precise and detailed approach to risk analysis and decision-making than traditional methods, which is particularly beneficial in environments with limited transparency and higher unpredictability (Sarah Lee 2025a). This allows for a more accurate assessment of potential errors in cash flow forecasts, prediction of corporate treasury growth under various scenarios, and optimization of investment decisions by identifying associated risks.

3. Methodology

3.1 Research Design

The study employs a simulation-based computational research design. This approach is analytical, relying on the robust statistical modeling of historical return data to project future fund performance through computational simulation. Unlike experimental or survey-based data collection, this design focuses on quantitative analysis and probabilistic forecasting. This computational design is particularly well-suited for financial market analysis where complex interactions and uncertainties necessitate probabilistic modeling to generate a comprehensive range of potential outcomes, rather than relying on single deterministic predictions.

3.2 Dataset and Data Preprocessing

The analysis utilizes a curated dataset of monthly Effective Annual Rate (EAR) values for all Kenyan Money Market Funds (MMFs) spanning from November 2017 to December 2024, (Kabui, Charles 2024). This dataset was compiled, cleaned, and processed and published on October 4, 2024, with its last modification on December 22, 2024. Data collection involved automated web crawling of Capital Markets Authority (CMA) and Cytonn Research reports. This comprehensive approach to data acquisition contributes to improving transparency within Kenya’s collective investment landscape and serves as a reliable resource for academic and market research.

The dataset also included supplementary details on Assets Under Management (AUM); however, AUM values were intentionally excluded from the current analysis to maintain a focused examination purely on the return behavior of the MMFs. It is important to note that data completeness varied across schemes due to differences in their inception dates and reporting practices.

To ensure statistical reliability and the integrity of the simulation, a rigorous data preprocessing procedure was followed:

- MMFs with insufficient historical data were identified and excluded from the analysis. This step was crucial to prevent unreliable statistical inferences that could arise from limited data points.

- The remaining data was systematically grouped by scheme, and all

NaN(Not a Number) values, representing missing or invalid entries, were cleaned to ensure a complete and consistent dataset for each fund. - As previously mentioned, Assets Under Management (AUM) data was deliberately excluded to narrow the focus of the study to the dynamics of return behavior, avoiding confounding variables related to fund size or operational scale

3.3 Monte Carlo Simulation Procedure

Monte Carlo simulation was systematically employed to generate probabilistic return distributions for each eligible MMF scheme. The procedure was meticulously designed to model future return paths based on historical performance, thereby capturing the inherent uncertainty in financial markets. The following steps detail the simulation process:

Compute Scheme-Specific Parameters: For each MMF scheme, the historical mean (\(\mu\)) and standard deviation (\(\sigma\)) of the Effective Annual Rate (EAR) values were calculated. These parameters are critical as they define the central tendency and dispersion of historical returns, serving as the basis for projecting future behavior.

Convert Annual to Monthly Parameters: The calculated annual mean (\(\mu\)) and standard deviation (\(\sigma\)) of EAR were converted to their monthly equivalents. This conversion is necessary because the simulation models monthly return paths. The monthly mean (\(\mu_{monthly}\)) was derived using the formula for compounding: \[ \mu_{monthly} = (1 + \mu / 100)^{(1/12)} − 1 \]

The monthly standard deviation (\(\sigma_{monthly}\)) was approximated by dividing the annual standard deviation by the square root of 12 (number of months in a year) and converting to decimal: \[ \sigma_{monthly} = \sigma / \sqrt{12} / 100 \]

This adjustment ensures that the simulated monthly volatility is consistent with the observed annual volatility.

- Simulate Return Paths: Using the NumPy library in Python,

1,000possible return paths were generated for each MMF over a 12-month horizon (equivalent to one year). These paths were generated based on a normal distribution, parameterized by the calculated monthly mean (\(\mu_{monthly}\)) and monthly standard deviation (\(\sigma_{monthly}\)). The formula used was:

simulated_paths = np.random.normal(mu_monthly, sigma_monthly, size=(1000, 12))This step creates a diverse set of hypothetical future scenarios, reflecting the probabilistic nature of financial returns.

- Calculate Cumulative Annual Returns: The simulated monthly returns for each path were compounded to obtain 1-year cumulative return outcomes. The compounding formula applied was:

cumulative_returns = (1 + simulated_paths).prod(axis=1) - 1This step aggregates the monthly simulations into a single annual return figure for each of the 1,000 paths, providing a distribution of potential annual returns for each fund. The results were then stored as percentages for ease of interpretation.

This systematic procedure allows for the generation of a comprehensive distribution of potential future returns for each MMF, moving beyond simple historical averages to incorporate the inherent uncertainty and variability that characterize financial markets.

3.4 Visualization and Comparative Analysis Techniques

To effectively communicate the complex probabilistic outcomes of the Monte Carlo simulation and facilitate a nuanced understanding of MMF performance, specific visualization and comparative analysis techniques were employed.

The primary visualization tool utilized was boxplots, generated using Matplotlib. Boxplots are particularly effective for displaying the spread and distribution of 1-year simulated returns for each MMF scheme. A boxplot visually represents the median, interquartile range (IQR), and potential outliers of a dataset. The “box” itself spans from the first quartile (25th percentile) to the third quartile (75th percentile), indicating the central 50% of the data. The line within the box marks the median (50th percentile), which represents the typical return. The “whiskers” extend from the box to indicate the variability outside the interquartile range, and individual points beyond the whiskers are often plotted as outliers. This visualization allows for an immediate qualitative comparison of the central tendency, dispersion, and skewness of returns across different MMFs, providing a clear picture of their potential performance ranges and volatility.

For a more quantitative and precise comparison of risk-return profiles, descriptive statistics were computed from the simulated return distributions. Key statistics included:

- Median Return: This metric provides a robust measure of central tendency, less susceptible to extreme values than the mean, representing the typical return an investor might expect.

- 25th and 75th Percentiles (Interquartile Range): These values delineate the middle 50% of the simulated returns, offering a clear indication of the typical spread and consistency of a fund’s performance. A narrower interquartile range generally suggests lower volatility and more predictable returns.

- 5th Percentile: This critical metric quantifies downside risk, indicating the return below which only 5% of simulated outcomes fall. For risk-averse investors, a higher 5th percentile is highly desirable, as it suggests a lower probability of significant losses.

The summary statistics were rounded to one decimal place for readability and sorted by median return in descending order to easily identify top-performing funds. This combination of simulation and visual analytics, complemented by precise statistical measures, enables a significantly more nuanced understanding of return volatility and downside exposure across different MMFs compared to traditional single-point estimates. It allows investors to assess risk-adjusted outcomes and make more informed decisions by considering the full distribution of potential returns.

4. Results

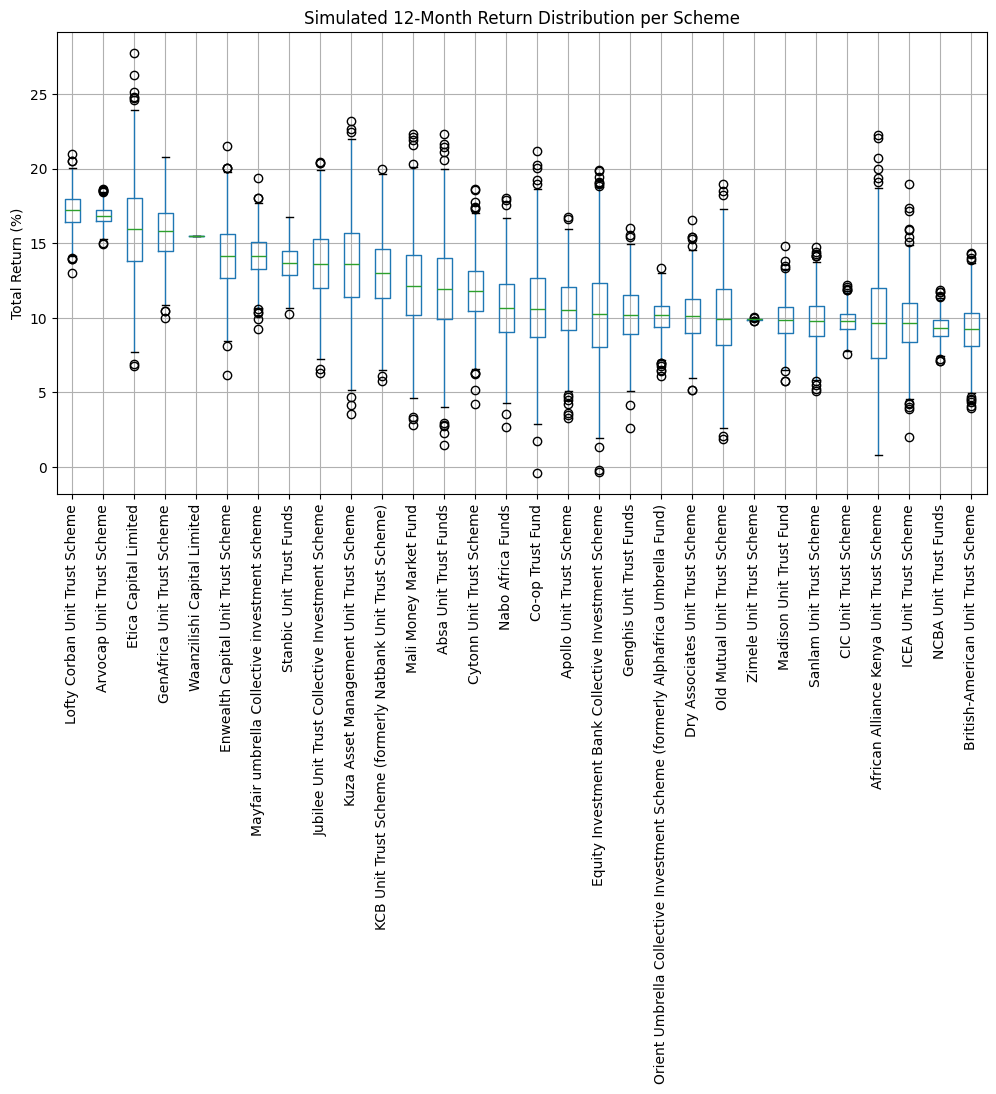

4.1 Boxplot Visualization of Simulated 12-Month Returns

The Monte Carlo simulation produced 1,000 possible 12-month return paths for 30 Money Market Fund (MMF) schemes in Kenya. These simulated returns were then visualized using boxplots, providing a comprehensive graphical representation of their respective distributions. The boxplot visualization, titled “Simulated 12-Month Return Distribution per Scheme,” illustrates the median, interquartile range, and overall spread of potential returns for each fund.

# Load the dataset

dataset = load_dataset(

path = "ToKnow-ai/Kenyan-Collective-Investment-Schemes-Dataset",

name = "Processed Investment Schemes Records",

split = 'data')

# Convert to pandas DataFrame

df = dataset.to_pandas()

for index, label in enumerate(dataset.features['entry_type'].names):

df['entry_type'] = df['entry_type'].replace(index, label)

df.tail(10)| entry_type | entry_date | entry_value | entry_scheme | |

|---|---|---|---|---|

| 86848 | EFFECTIVE_ANNUAL_RATE | 2024-12-22 | 13.0 | ICEA Unit Trust Scheme |

| 86849 | EFFECTIVE_ANNUAL_RATE | 2024-12-22 | 12.7 | CIC Unit Trust Scheme |

| 86850 | EFFECTIVE_ANNUAL_RATE | 2024-12-22 | 12.7 | Absa Unit Trust Funds |

| 86851 | EFFECTIVE_ANNUAL_RATE | 2024-12-22 | 12.5 | Mayfair umbrella Collective investment scheme |

| 86852 | EFFECTIVE_ANNUAL_RATE | 2024-12-22 | 12.2 | African Alliance Kenya Unit Trust Scheme |

| 86853 | EFFECTIVE_ANNUAL_RATE | 2024-12-22 | 12.2 | Ziidi Money Market Fund |

| 86854 | EFFECTIVE_ANNUAL_RATE | 2024-12-22 | 11.8 | Stanbic Unit Trust Funds |

| 86855 | EFFECTIVE_ANNUAL_RATE | 2024-12-22 | 8.5 | Equity Investment Bank Collective Investment S... |

| 86856 | EFFECTIVE_ANNUAL_RATE | 2024-12-22 | 13.9 | Dry Associates Unit Trust Scheme |

| 86857 | EFFECTIVE_ANNUAL_RATE | 2024-12-22 | 17.1 | Cytonn Unit Trust Scheme |

group_df = df.groupby(['entry_scheme', 'entry_type'])

months = 12

simulations = 1000

entry_schemes = df['entry_scheme'].unique()

results = {}

for entry_scheme in entry_schemes:

if (entry_scheme, 'EFFECTIVE_ANNUAL_RATE') not in group_df.groups:

continue

ear_data = group_df.get_group(

(entry_scheme, 'EFFECTIVE_ANNUAL_RATE'))["entry_value"].dropna()

if len(ear_data) < 6:

continue # not enough history

mu = ear_data.mean()

sigma = ear_data.std()

# Convert EAR mean and std deviation (annual %) to monthly decimal

mu_monthly = (1 + mu / 100) ** (1 / 12) - 1

sigma_monthly = sigma / np.sqrt(12) / 100

# Simulate 12 months of returns

simulated_paths = np.random.normal(

mu_monthly, sigma_monthly, size=(simulations, months))

# Compound returns over 12 months

cumulative_returns = (1 + simulated_paths).prod(axis=1) - 1

# Store in results as percentage

results[entry_scheme] = cumulative_returns * 100

simulated_df = pd.DataFrame(results)

# Calculate medians per scheme (column)

medians = simulated_df.median()

# Sort columns by median descending

sorted_columns = medians.sort_values(ascending=False).index

# Reorder simulated_df

sorted_simulated_df = simulated_df[sorted_columns]

# Plot sorted boxplot

sorted_simulated_df.boxplot(rot=90, figsize=(12, 6))

plt.title("Simulated 12-Month Return Distribution per Scheme")

plt.ylabel("Total Return (%)")

plt.show()

4.2 Summary Statistics of Simulated Returns

To complement the visual insights from the boxplots, detailed summary statistics were computed for the simulated 12-month returns of each MMF scheme. These statistics provide quantitative measures of central tendency, dispersion, and downside risk, enabling a precise comparison of fund performance. The table below presents the median, 25th percentile, 75th percentile, and 5th percentile for each scheme, sorted by median return in descending order.

# Compute symmary statistic

summary_stats = pd.DataFrame({

'Scheme': simulated_df.columns,

'Median (%)': simulated_df.median(),

'25th (%)': simulated_df.quantile(0.25),

'75th (%)': simulated_df.quantile(0.75),

'5th (%)': simulated_df.quantile(0.05)

})

# Round values for readability

summary_stats = summary_stats.round(1)

# Sort by Median if desired

summary_stats = summary_stats.sort_values(

by='Median (%)', ascending=False).reset_index(drop=True)

# Display top result

summary_stats.head(30)| Scheme | Median (%) | 25th (%) | 75th (%) | 5th (%) | |

|---|---|---|---|---|---|

| 0 | Lofty Corban Unit Trust Scheme | 17.2 | 16.5 | 18.0 | 15.2 |

| 1 | Arvocap Unit Trust Scheme | 16.9 | 16.5 | 17.2 | 15.9 |

| 2 | GenAfrica Unit Trust Scheme | 15.9 | 14.6 | 17.1 | 12.9 |

| 3 | Etica Capital Limited | 15.8 | 13.5 | 17.8 | 10.3 |

| 4 | Waanzilishi Capital Limited | 15.5 | 15.5 | 15.5 | 15.5 |

| 5 | Mayfair umbrella Collective investment scheme | 14.2 | 13.2 | 15.2 | 11.9 |

| 6 | Enwealth Capital Unit Trust Scheme | 14.0 | 12.7 | 15.5 | 10.7 |

| 7 | Kuza Asset Management Unit Trust Scheme | 13.8 | 11.4 | 16.0 | 8.6 |

| 8 | Stanbic Unit Trust Funds | 13.7 | 12.9 | 14.5 | 11.7 |

| 9 | Jubilee Unit Trust Collective Investment Scheme | 13.7 | 12.1 | 15.1 | 9.9 |

| 10 | KCB Unit Trust Scheme (formerly Natbank Unit T... | 12.9 | 11.2 | 14.7 | 9.1 |

| 11 | Mali Money Market Fund | 12.3 | 10.2 | 14.7 | 7.3 |

| 12 | Absa Unit Trust Funds | 11.8 | 9.8 | 14.0 | 6.7 |

| 13 | Cytonn Unit Trust Scheme | 11.7 | 10.3 | 13.2 | 8.2 |

| 14 | Nabo Africa Funds | 10.7 | 9.2 | 12.2 | 7.0 |

| 15 | Apollo Unit Trust Scheme | 10.6 | 9.2 | 12.3 | 7.1 |

| 16 | Co-op Trust Fund | 10.6 | 8.6 | 12.5 | 5.7 |

| 17 | Dry Associates Unit Trust Scheme | 10.2 | 9.0 | 11.5 | 7.3 |

| 18 | Genghis Unit Trust Funds | 10.1 | 8.8 | 11.4 | 7.2 |

| 19 | Equity Investment Bank Collective Investment S... | 10.1 | 8.1 | 12.3 | 5.2 |

| 20 | Orient Umbrella Collective Investment Scheme (... | 10.0 | 9.3 | 10.8 | 8.2 |

| 21 | Madison Unit Trust Fund | 9.9 | 9.0 | 10.8 | 7.8 |

| 22 | Zimele Unit Trust Scheme | 9.9 | 9.9 | 9.9 | 9.8 |

| 23 | CIC Unit Trust Scheme | 9.8 | 9.3 | 10.3 | 8.6 |

| 24 | ICEA Unit Trust Scheme | 9.7 | 8.4 | 11.1 | 6.4 |

| 25 | Old Mutual Unit Trust Scheme | 9.7 | 7.7 | 11.8 | 5.1 |

| 26 | Sanlam Unit Trust Scheme | 9.7 | 8.7 | 10.7 | 7.3 |

| 27 | African Alliance Kenya Unit Trust Scheme | 9.5 | 7.2 | 12.0 | 4.1 |

| 28 | NCBA Unit Trust Funds | 9.3 | 8.8 | 9.9 | 8.0 |

| 29 | British-American Unit Trust Scheme | 9.1 | 8.0 | 10.3 | 6.1 |

4.3 Key Observations from the Simulation Results

The Monte Carlo simulations revealed distinct return profiles among the 30 Money Market Fund (MMF) schemes in Kenya, offering a granular view beyond simple average returns. Several important patterns emerged from the updated summary statistics and boxplot visualizations:

Top Performing Funds by Median Return:

- Lofty Corban Unit Trust Scheme demonstrated the highest simulated median annual return at

17.2%, followed closely by Arvocap Unit Trust Scheme at16.9%. These funds also exhibited relatively narrow percentile ranges, particularly evident in Arvocap’s tight spread (16.5%to17.2%between the 25th and 75th percentiles), suggesting both high performance and a notable degree of stability. This combination of high returns and low variability makes them particularly attractive for investors prioritizing consistent growth. - Etica Capital Limited and GenAfrica Unit Trust Scheme achieved strong median returns of

15.8%. However, their wider spreads between the 25th and 75th percentiles (e.g., Etica:13.5%to17.8%) indicate higher volatility compared to Lofty Corban and Arvocap, implying greater potential for both higher gains and larger fluctuations. - Waanzilishi Capital Limited reported a highly compressed distribution, with identical values for all percentiles (

15.5%). This flat distribution raises concerns about the underlying historical return series, suggesting it might be static or incomplete, as genuine market-driven returns typically exhibit some degree of variability.

Lower Performing Funds:

- At the lower end of the rankings, NCBA Unit Trust Funds and British-American Unit Trust Scheme showed median returns of

9.3%. These funds generally exhibited relatively tight distributions (e.g., NCBA:8.8%to9.9%), reflecting a pattern of lower but more stable performance. For investors with a very low-risk appetite, such funds might be considered for capital preservation, even if returns are modest. - African Alliance Kenya Unit Trust Scheme presented one of the widest spreads among the lower-performing funds, with a median of

9.7%but a 5th percentile as low as4.1%. This wide range, especially the low 5th percentile, suggests significant downside risk, indicating that while the median return is near the average, there is a non-trivial probability of experiencing substantially lower returns.

Notable Patterns:

- Data Quality Indicators: Several schemes, such as Zimele Unit Trust Scheme and Waanzilishi Capital Limited, displayed zero or near-zero variance across their simulated returns. Zimele, for instance, showed a median of 9.9% with 25th, 75th, and 5th percentiles all at

9.9%or9.8%. This lack of variability strongly suggests issues with stale, incomplete, or potentially synthetic historical data, which can significantly impact the reliability of any simulation-based analysis. Such observations highlight the critical importance of robust data quality checks in financial modeling. - Balance of Return and Risk: Funds like Kuza Asset Management Unit Trust Scheme, Enwealth Capital Unit Trust Scheme, and Mayfair umbrella Collective investment scheme offered solid median returns (ranging from

13.8%to14.2%) with moderate variability. For example, Kuza’s 5th percentile was8.6%, indicating a reasonable downside protection despite a wider interquartile range. These funds potentially offer a good balance between achieving competitive returns and managing risk, appealing to a broader range of investors who seek more than just capital preservation but are still risk-averse.

These observations collectively demonstrate that relying solely on average EARs would provide an incomplete and potentially misleading picture of MMF performance. The distributional insights derived from Monte Carlo simulation reveal crucial differences in risk exposure and return consistency across funds, empowering investors to make more informed and risk-adjusted decisions.

5. Discussion

5.1 Interpreting Risk-Return Trade-offs in Kenyan MMFs

The simulation results provide a nuanced perspective on the risk-return trade-offs prevalent within Kenyan Money Market Funds, moving beyond the simplistic view offered by traditional metrics. While MMFs are generally considered low-risk instruments, the analysis reveals significant variability in their performance profiles, underscoring that even within this asset class, higher returns are often accompanied by greater volatility and potential for downside risk.

Funds such as Lofty Corban Unit Trust Scheme and Arvocap Unit Trust Scheme demonstrated both high median returns (17.2% and 16.9% respectively) and relatively narrow percentile ranges, particularly Arvocap’s tight distribution. This combination suggests that these funds have historically managed to deliver superior returns with a degree of consistency, making them attractive for investors seeking strong performance without excessive volatility. Their narrow spreads indicate a lower probability of significant deviations from their median return.

Conversely, funds like Etica Capital Limited and Kuza Asset Management Unit Trust Scheme also exhibited elevated median performance (15.8% and 13.8%respectively) but were characterized by wider interquartile ranges and lower 5th percentile values. For example, Etica’s 5th percentile was 10.3%, and Kuza’s was 8.6%. This pattern indicates increased downside potential, meaning that while these funds might offer higher average returns, investors face a greater probability of experiencing returns significantly below the median. This highlights a classic risk-return trade-off: pursuing higher potential gains often entails accepting a broader range of possible outcomes, including less favorable ones.

For risk-averse investors, the stability and consistency of returns are paramount. Funds like Stanbic Unit Trust Funds and Arvocap Unit Trust Scheme (despite its higher median) offer strong returns (13.7% and 16.8% respectively) with relatively narrow spreads. This makes them appealing to those prioritizing capital preservation and predictable income over maximizing absolute returns. The 5th percentile, in particular, becomes a crucial metric for such investors, as it provides a quantifiable measure of the worst-case scenario within a high degree of confidence. A fund with a higher 5th percentile, even if its median is slightly lower, may be preferred by investors who are more concerned about avoiding losses than achieving maximum gains, aligning with the concept of loss aversion in behavioral finance.

The analysis also revealed funds like African Alliance Kenya Unit Trust Scheme, which, despite a median return of 9.5%, had a notably low 5th percentile of 4.1%. This wide spread and significant downside exposure indicate that while the fund might appear average based on its median, it carries substantial risk of underperforming expectations, which would not be evident from a simple EAR figure. This emphasizes that investors must consider the entire distribution of potential returns to accurately assess the risk-adjusted performance of an MMF.

5.2 The Power of Distributional Insight for Informed Investment Decisions

This study strongly confirms that Monte Carlo simulation adds substantial value to the evaluation of financial instruments, even for those traditionally considered low-volatility like Money Market Funds. The primary strength of this approach lies in its ability to capture the full return distribution, providing investors with a deeper and more realistic understanding of potential outcomes than traditional single-point estimates.

Traditional metrics, such as trailing EAR or average annual return, inherently fail to expose hidden risks or accurately convey performance stability. For instance, an MMF might report a high average EAR, leading investors to believe it is consistently top-performing. However, the simulation can reveal that this average is achieved through significant volatility, with a high probability of both very high and very low returns. This is precisely where distributional insight becomes invaluable. By visualizing the spread of returns through boxplots and quantifying it with percentiles (e.g., 25th, 75th, and 5th percentiles), investors gain a comprehensive view of the fund’s risk profile.

The 5th percentile, in particular, serves as a critical indicator of downside risk, providing a quantifiable measure of potential losses that is absent from average return figures. For a risk-averse investor, knowing that a fund’s return is unlikely to fall below a certain threshold (e.g., 5th percentile) offers a more robust basis for decision-making than simply observing its median return. This allows investors to align their choices with their actual risk tolerance and capital preservation goals, rather than being misled by headline figures.

Furthermore, understanding the full distribution helps mitigate behavioral biases that often influence investment decisions. For example, herd mentality, where investors follow popular trends, can be challenged by presenting a clear picture of the underlying volatility and downside potential of a “hot” fund. Similarly, overconfidence, which can lead to underestimation of risk, is addressed by explicitly showing the range of possible outcomes, including less favorable ones. By providing a probabilistic framework, the Monte Carlo simulation encourages a more rational and data-driven approach, fostering a deeper understanding of market dynamics and the inherent uncertainties.

Ultimately, the findings support the integration of risk-aware simulation techniques into everyday fund comparison tools. These methods are lightweight, transparent, and significantly more informative than relying on historical EAR snapshots alone. They empower investors to assess risk-adjusted outcomes, leading to more resilient and informed investment strategies in the dynamic financial landscape of Kenya.

5.3 Implications of Data Quality for Financial Modeling in Emerging Markets

The simulation results highlighted a critical aspect of financial modeling in emerging markets: the paramount importance of data quality and completeness. The observation of flat or suspiciously low-variance return profiles for certain schemes, such as Waanzilishi Capital Limited and Zimele Unit Trust Scheme, directly points to potential issues with the underlying historical data.

When a fund’s simulated return distribution shows little to no variability (e.g., identical values for median, 25th, 75th, and 5th percentiles), it suggests that the historical data used to derive the mean and standard deviation might be stale, incomplete, or even synthetic. In a dynamic financial market, even for relatively low-volatility instruments like MMFs, some degree of fluctuation in returns is expected due to changing interest rates, macroeconomic conditions, and fund management decisions. A lack of such variability in historical data can lead to an artificially narrow, and therefore misleading, simulated distribution.

This phenomenon has several significant implications for financial modeling and investor decision-making in emerging markets:

- Reliability of Projections: If the input data does not accurately reflect the true historical variability of a fund, any simulation built upon it will produce unreliable projections. This can lead investors to misjudge the actual risk and return characteristics of a fund, potentially making decisions based on flawed assumptions.

- Transparency and Trust: The presence of such data anomalies can erode trust in publicly available financial information. For regulators and market participants, it underscores the need for enhanced data reporting standards and more rigorous validation processes.

- Challenges in Emerging Markets: Emerging markets often face unique challenges in data transparency and availability compared to more developed markets. Economic, political, and social risks can be significant, and the unique cultural and regulatory environments can make it difficult to obtain accurate and consistent market data for valuation purposes. This makes robust data preprocessing and critical assessment of data sources even more crucial.

- Methodological Robustness: While Monte Carlo simulation is a powerful tool, its effectiveness is inherently tied to the quality of the input data. The principle that “the outcomes generated by the simulation follow a normal distribution, forming a bell curve. However, the simulation assumes a perfectly efficient market and neglects external factors influencing price movements” means that if the historical data itself is flawed, the resulting bell curve may not accurately represent true market behavior.

Therefore, this study’s findings serve as a flag for data quality issues, emphasizing that even with advanced simulation techniques, the integrity of the input data remains foundational. Future research and practical applications in emerging markets must prioritize rigorous data validation and, where necessary, explore methods to impute or adjust for missing or anomalous historical data to ensure the reliability and validity of financial models.

5.4 Broader Context: Kenyan MMFs within the National and Regional Financial Ecosystem

Kenyan Money Market Funds operate within a dynamic national and regional financial ecosystem, influenced by macroeconomic conditions, regulatory frameworks, and technological advancements. Their increasing prominence reflects broader trends in financial deepening and inclusion within East Africa.

Macroeconomic and Regulatory Environment: The Central Bank of Kenya (CBK) plays a pivotal role in shaping the financial markets through its monetary policy implementation, management of foreign exchange reserves, and domestic debt management. These functions directly impact interest rates and liquidity, which in turn influence the yields offered by MMFs. For instance, a decline in Treasury bill rates directly affects MMF returns given their significant investment in short-term government securities. The Capital Markets Authority (CMA) provides regulatory oversight, ensuring MMFs adhere to investment guidelines.

Financial Inclusion and Digital Transformation: A significant driver of MMF growth in Kenya is the pervasive mobile money ecosystem, particularly M-PESA. Initiatives like the Ziidi Money Market Fund, a partnership between Safaricom and fund managers, exemplify how digital platforms are democratizing access to investment products. With minimum investments as low as KES 100 and instant withdrawals via M-PESA, these mobile-first MMFs have attracted hundreds of thousands of new investors, significantly enhancing financial inclusion for previously underserved populations. This aligns with the government’s bottom-up economic transformation agenda by enabling low and mid-income earners to participate in wealth creation. The ability to earn daily compounded interest and the transparency of daily interest rates further incentivize participation.

Investor Behavior and Market Dynamics: Kenyan investors increasingly view MMFs as a preferred savings vehicle for emergency funds and short-term goals due to their capital preservation focus and liquidity. However, the analysis highlights that even within MMFs, investors face choices with varying risk-return profiles. The observed responsiveness of fund inflows to yields can create incentives for fund managers to take on more risk, as seen in global contexts during financial crises. This dynamic, coupled with the potential for behavioral biases, necessitates robust analytical tools like Monte Carlo simulation to provide a clearer, risk-adjusted view of performance.

Comparison with Other Investment Avenues: While MMFs offer competitive returns compared to bank savings accounts, their real returns can be impacted by inflation. For example, with Kenya’s 2025 inflation at 3.8% in May 2025 (Kenya National Bureau of Statistics 2025), a 10-12% average MMF return translates to a real return of approximately 7.2%. This suggests that while MMFs are excellent for short-term capital preservation and liquidity, they may not be sufficient for long-term wealth creation that significantly outpaces inflation. Diversification across different asset classes, including real estate and government securities remains crucial for maximizing returns and minimizing systematic risk over longer horizons.

In essence, Kenyan MMFs are not isolated financial products but integral components of a rapidly evolving financial landscape. Their growth is intertwined with digital innovation, regulatory oversight, and shifting investor preferences, making a nuanced, risk-aware evaluation essential for sustainable financial development.

5.5 Comparison with Global and Emerging Market Trends in MMF Performance and Risk

The performance and risk characteristics of Kenyan MMFs, as revealed by this study, resonate with broader global and emerging market trends, while also exhibiting unique local nuances.

Global MMF Industry Growth and Structure: The significant growth of Kenyan MMFs, with AUM reaching Kshs 246.8 billion by Q4’2024 and a 5-year CAGR of 31.8% (Cytonn Research 2025), mirrors the global expansion of the MMF industry to over USD 7.4 trillion (J.P. Morgan Asset Management 2023). This global trend is driven by both institutional and retail investors seeking liquidity and capital preservation. The structure of Kenyan MMFs, investing in short-term, high-quality debt instruments like Treasury bills and commercial paper, aligns with international norms.

Risk-Taking Incentives and Vulnerability: Globally, MMFs have historically been perceived as safe, almost cash-like investments. However, the 2008 financial crisis exposed their vulnerabilities, particularly their incentives to take on risk due to fund inflows being highly responsive to yields. This led to an unprecedented expansion of risk-taking opportunities as spreads between risky and safe instruments widened. While Kenyan MMFs are less volatile than their global counterparts, the observed variability in simulated returns and the presence of funds with wider downside spreads suggest that similar risk-taking incentives, though perhaps less pronounced, may exist. The flat distributions observed for some Kenyan funds could also be indicative of data issues that mask underlying risks.

Challenges in Emerging Market Evaluation: Evaluating MMFs in emerging markets presents unique challenges that resonate across academic studies. These include economic instability, limited access to capital, and the need for robust risk management strategies. The difficulty in obtaining accurate market data and the potential for significant economic, political, and social risks in these regions make traditional valuation methods less reliable. Assumptions underpinning conventional financial models, such as the efficient market hypothesis, may not hold true in emerging markets, necessitating alternative approaches. This study’s use of Monte Carlo simulation directly addresses these challenges by providing a probabilistic framework that can model complex systems and quantify uncertainty, a recognized benefit in emerging market finance.

Role in Financial Inclusion: The role of MMFs in driving financial inclusion is a shared trend across many emerging economies. The success of mobile-integrated MMFs in Kenya, such as Ziidi MMF, which allows micro-investments and instant access via M-PESA, exemplifies how fintech innovations are bridging the gap between traditional financial services and underserved populations. This aligns with broader efforts to empower local entrepreneurs and stimulate economic growth by improving access to capital and fostering financial literacy.

In summary, Kenyan MMFs are part of a global financial phenomenon, adapting to local market conditions and leveraging technological advancements to expand financial access. However, they also share common challenges with other emerging markets, particularly regarding data quality and the need for sophisticated risk assessment tools that move beyond simplistic metrics to provide a true picture of risk-adjusted performance.

6. Conclusion and Recommendations

6.1 Conclusion

This study demonstrates the effectiveness of Monte Carlo simulation in evaluating the performance of Money Market Fund (MMF) schemes under uncertainty. By modeling 1,000 possible future return paths per fund using historical EAR data, the analysis captures both expected returns and the variability around them - providing a richer, distribution-based perspective on performance.

Key conclusions include:

- Return variability across MMFs is significant, even when average EARs appear similar. Some funds offer higher potential returns but with greater downside risk

- Median return alone is insufficient as a decision metric. Distributional characteristics such as the 5th percentile or interquartile range reveal crucial risk exposures

- Probabilistic modeling enables more informed investment decisions by allowing investors to assess risk-adjusted outcomes rather than relying on point estimates

- The simulation framework is lightweight and fully reproducible using open-source tools like NumPy and pandas, making it suitable for both institutional and retail applications

6.2 Recommendations

- For Investors: Consider both median and lower-percentile returns when selecting MMFs. Funds with moderate but consistent performance may be more suitable for capital preservation goals.

- For Financial Advisors: Use simulation-based visualizations (e.g., boxplots, risk-return maps) to communicate risk profiles to clients. This can help steer conversations beyond headline EARs toward more robust decision-making.

- For Fund Managers: Enhance transparency by reporting not only historical returns but also metrics like volatility, simulated downside risk, and range of possible outcomes.

- For Researchers and Developers: Extend this framework to include macroeconomic variables (e.g., interest rate trends), fund-specific strategies, or peer clustering to develop more nuanced fund comparison models.

6.3 Limitations

While the Monte Carlo simulation approach offers a more nuanced and risk-aware evaluation of Money Market Funds (MMFs), several limitations must be acknowledged:

- Assumption of Normally Distributed Returns

The simulation assumes that monthly EARs follow a normal distribution. In practice, financial return distributions can be skewed or fat-tailed, especially in turbulent market conditions. This assumption may understate the likelihood of extreme events (i.e., tail risk).

- Dependence on Historical Data

The simulation relies entirely on past EAR values. This approach assumes that historical patterns will persist, which may not hold true during regime shifts, interest rate shocks, or macroeconomic disruptions.

- Exclusion of AUM and Portfolio Composition

This study focused purely on return behavior and did not consider Assets Under Management (AUM) or fund asset allocation. Larger funds may benefit from economies of scale or more diversified portfolios—factors that can affect performance stability and liquidity.

- Static Simulation Horizon

All simulations were conducted over a 12-month horizon. While this is practical for annual return analysis, investors with shorter or longer investment timelines may require customized modeling to capture different risk dynamics.

- Data Quality and Completeness

Some schemes exhibited flat or suspiciously low-variance return profiles, possibly due to stale, incomplete data. Although schemes with insufficient data were excluded, the quality of publicly disclosed EAR figures can still affect simulation reliability.

- Simplified Risk Metrics

This analysis focused on percentile-based statistics and did not incorporate formal risk-adjusted metrics like Sharpe Ratio, Sortino Ratio, or Conditional Value at Risk (CVaR), which may be useful in further evaluation.

7. References

Auerbach, Michael P. 2021. ‘Money Markets’. https://www.ebsco.com/research-starters/business-and-management/money-markets.

Cytonn Research. 2024. ‘Q2’2024 Unit Trust Funds Performance Note’. https://cytonn.com/topicals/q22024-unit-trust-1.

———. 2025. ‘Q4’2024 Unit Trust Funds Performance Note’. https://cytonn.com/uploads/downloads/q42024-utf-performance-notevf6.pdf.

Dave. 2024. ‘What are the limitations of using the accounting rate of return (ARR) method?’ TutorChase. https://www.tutorchase.com/answers/ib/business-management/what-are-the-limitations-of-using-the-accounting-rate-of-return--arr--method.

Ejiofor, Chinelo, and Rita Attah. 2023. ‘Financial Management Strategies in Emerging Markets: A Review of Theoretical Models and Practical Applications’. Magna Scientia Advanced Research and Reviews 7 (April): 123–40. https://doi.org/10.30574/msarr.2023.7.2.0054.

Jerry Grzegorzek. 2022. ‘Average Rate of Return (ARR) of An Investment’. https://www.superbusinessmanager.com/average-rate-of-return-arr-of-an-investment/.

J.P. Morgan Asset Management. 2023. ‘Introduction to Money Market Funds and Ultra-Short Duration Strategies’. https://am.jpmorgan.com/content/dam/jpm-am-aem/global/en/liq/literature/brochure/introduction-to-mmfs.pdf.

Kabui, Charles. 2024. ‘Kenyan Collective Investment Schemes Dataset’. https://toknow.ai/posts/kenyan-collective-investment-schemes-dataset/index.html.

Kacperczyk, Marcin, and Philipp Schnabl. 2013. ‘How Safe Are Money Market Funds?’ https://pages.stern.nyu.edu/~pschnabl/research/KacperczykSchnabl2013.pdf.

Kenton, Will. 2025. ‘Monte Carlo Simulation: What It Is, How It Works, History, 4 Key Steps’. https://www.investopedia.com/terms/m/montecarlosimulation.asp.

Kenya National Bureau of Statistics. 2025. ‘Consumer Price Indices and Inflation Rates - May 2025’. https://www.knbs.or.ke/reports/consumer-price-indices-and-inflation-rates-may-2025/.

KPMG Ghana. 2024. ‘Beyond DCF: Enhancing Business Valuation in Emerging Markets through Monte Carlo Simulation Techniques’. https://assets.kpmg.com/content/dam/kpmg/gh/pdf/Thought%20Leadership%20-%20Monte%20Carlo.pdf.

Lofty-Corban. 2025. ‘Why Are Money Market Fund Rates Declining in Kenya?’ https://loftycorban.com/?p=7104.

Pavlik, Martin, and Grzegorz Michalski. 2025. ‘Monte Carlo Simulations for Resolving Verifiability Paradoxes in Forecast Risk Management and Corporate Treasury Applications’. International Journal of Financial Studies 13 (2). https://doi.org/10.3390/ijfs13020049.

Raymond A. Mason School of Business. 2025. ‘5 Behavioral Biases That Can Impact Your Investing Decisions’. https://online.mason.wm.edu/blog/behavioral-biases-that-can-impact-investing-decisions.

Safaricom. 2024. ‘Ziidi Money Market Fund (MMF) by Safaricom)’. https://www.safaricom.co.ke/main-mpesa/m-pesa-services/wealth/ziidi.

———. 2025. ‘Safaricom Partners with Investment Firms to Unveil Ziidi Money Market Fund Powered by m-PESA’. https://www.safaricom.co.ke/media-center-landing/press-releases/safaricom-partners-with-investment-firms-to-unveil-ziidi-money-market-fund-powered-by-m-pesa.

Sarah Lee. 2025a.‘ Deep Dive: Monte Carlo Simulation in Economics’. https://www.numberanalytics.com/blog/deep-dive-monte-carlo-simulation-economics.

———. 2025b. ‘EAR Demystified: A Guide to Effective Annual Rate’. https://www.numberanalytics.com/blog/ear-demystified-guide-effective-annual-rate.

Standard Investment Bank. 2025. ‘Press Release: Announcing the Launch of Ziidi MMF by Safaricom PLC & Managed by SIB’. https://sib.co.ke/press-release-announcing-the-launch-of-ziidi-mmf-by-safaricom-plc-managed-by-sib/.

Step by Step Insurance. 2025a. ‘Top Money Market Funds in Kenya 2025: Comparing the Best Providers - Step By Step Insurance — Stepbystepinsurance.co.ke’. https://stepbystepinsurance.co.ke/top-money-market-funds-in-kenya-2025-comparing-the-best-providers/.

———. 2025b. ‘Ziidi Money Market Fund Tops Ksh 6 Billion: What Kenyan Investors Need to Know’. https://stepbystepinsurance.co.ke/ziidi-money-market-fund-tops-ksh-6-billion-what-kenyan-investors-need-to-know/.

Xu, Tianyou. 2024b. ‘The Application of Monte Carlo Simulation for Risk and Behavior Analysis in Financial Markets’. Highlights in Business, Economics and Management 45 (December): 19–24. https://doi.org/10.54097/djgy6809.

———. 2024a. ‘The Application of Monte Carlo Simulation for Risk and Behavior Analysis in Financial Markets’. Highlights in Business, Economics and Management 45 (December): 19–24. https://doi.org/10.54097/djgy6809.

Disclaimer: For information only. Accuracy or completeness not guaranteed. Illegal use prohibited. Not professional advice or solicitation. Read more: /terms-of-service

Reuse

GNU GENERAL PUBLIC LICENSE v3.0(View License)

Citation

BibTeX citation:

@misc{kabui2025,

author = {{Kabui, Charles}},

title = {Efficiency and {Risk-Aware} {Performance} {Analysis} of

{Kenyan} {Money} {Market} {Funds} {Using} {Monte} {Carlo}

{Simulation:} {A} {Comprehensive} {Review} and {Empirical} {Study}},

date = {2025-06-10},

url = {https://toknow.ai/posts/computational-techniques-in-data-science/efficiency-and-risk-aware-comparison-of-money-market-fund-schemes-using-monte-carlo-simulation/index.html},

langid = {en-GB},

abstract = {This study presents a comprehensive, risk-aware

comparative performance analysis of Kenyan Money Market Funds (MMFs)

using Monte Carlo simulation. Traditional deterministic metrics,

such as Effective Annual Rates (EAR), often fail to capture the

crucial variability and underlying risk of returns, leading to

investor uncertainty regarding schemes offering consistent and

favorable risk-adjusted returns. This research addresses this gap by

providing a probabilistic framework. The general objective is to

evaluate and compare the risk-adjusted performance of Kenyan MMF

schemes by modeling future return scenarios over a one-year horizon.

The methodology involved preprocessing a curated dataset of monthly

EAR values for Kenyan MMFs from November 2017 to December 2024,

excluding funds with insufficient historical data. For each eligible

scheme, historical mean and standard deviation of EARs were computed

and converted to monthly equivalents. Subsequently, 1,000 possible

one-year return paths were simulated using a normal distribution,

and cumulative annual returns were calculated. Results were

visualized using boxplots and summarized with descriptive

statistics, including median, 25th, 75th, and 5th percentiles. Key

findings revealed distinct return profiles among MMFs. Funds like

Lofty Corban Unit Trust Scheme demonstrated high median returns

(17.2\%) with notable stability, while others, such as Etica Capital

Limited, showed strong medians (15.8\%) but with wider return

spreads, indicating higher volatility. The analysis also flagged

potential data quality issues for schemes exhibiting near-zero

variance. The study concludes that Monte Carlo simulation offers a

superior, distribution-based understanding of MMF performance,

empowering investors to make more informed, risk-aware decisions by

considering the full spectrum of potential outcomes beyond simple

averages. This approach is crucial for navigating the dynamic Kenyan

financial market. \textbackslash newpage}

}

For attribution, please cite this work as:

Kabui, Charles. 2025. “Efficiency and Risk-Aware Performance

Analysis of Kenyan Money Market Funds Using Monte Carlo Simulation: A

Comprehensive Review and Empirical Study.” https://toknow.ai/posts/computational-techniques-in-data-science/efficiency-and-risk-aware-comparison-of-money-market-fund-schemes-using-monte-carlo-simulation/index.html.